What are the Greatest Revenue Cycle Management Challenges?

“The front-end of the revenue cycle must be diligent with determining Medicaid eligibility and assist uninsured patients understand their coverage options with the insurance exchanges."

RevCycleIntelligence.com recently polled over 60 readers to assess revenue cycle management challenges and opportunities, from the front-end, to the back-end, and everything in between.

Readers said collecting payment from a patient in a timely and efficient manner is a top priority. But patients are struggling to pay and high (and higher) deductibles are hurting revenue cycle.

Another reader concern is related to ICD-10 preparation and confidence levels. Physician readiness levels are reportedly providers’ leading ICD-10 concern.

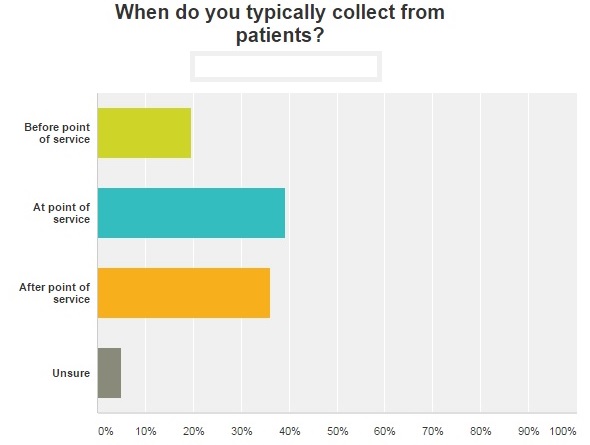

Why collection at or before point-of-service matters

When healthcare providers place greater emphasis on collecting from patients at or before point-of-service, their revenue reportedly improves.

Nine in ten physician practices and facilities concur that collecting patient financial responsibility before the patient leaves a physician’s office or hospital setting proves financially beneficial, according to an Avality Research Study.

Over 85 percent healthcare providers say collecting from patients after point-of-service is an arduous task, said Availity.

“[The] conversation with the patient has to start early – at or before the point of service – if providers are to reduce the amount of bad debt they’re currently experiencing,” stated Russ Thomas, Availity CEO, within a press release.

Patients are not always able to expediently pay their bills, confirms a report from PwC’s Health Research Institute.

“Research has found that as many as two out of three bankruptcies involve illness, injury, significant uncovered medical bills or a combination of these factors and the fallout from them,” the report states.

“The front-end of the revenue cycle must be diligent with determining Medicaid eligibility and assist uninsured patients understand their coverage options with the insurance exchanges,” explained Derek Bang, CPA, CGMA, Chief Innovation Officer at Crowe Horwath LLP, to RevCycleIntelligence.com.

“There must be greater focus on point-of-service cash collections, given the growing amount of patient responsibility for payment.”

Half of Xtelligent Media readers confirmed they were successfully collecting from patients at or before point-of-service. Over 1 in 3 reported they were generally collecting from patients after point-of-service.

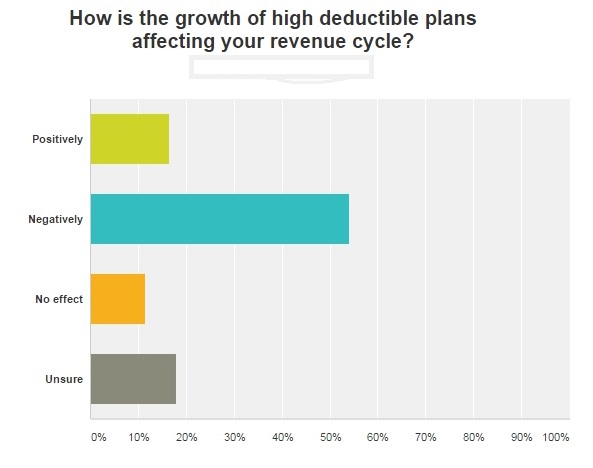

High-deductibles are hitting revenue cycle hard

Our readers’ revenue cycle was apparently being hit hard by the growth of high deductible plans. Fifty-four percent of those surveyed said their revenue cycle was detrimentally impacted. Eleven percent of readers asserted high deductible plan growth was neutrally impacting their revenue cycle. Sixteen percent said their revenue cycle reaped tangible benefits from high deductible plan expansion.

A recent surge in high deductible plans means patients are becoming a tad more discerning when selecting healthcare providers.

From 2003 to 2014, insurance premiums in every state nationwide rose nearly three times as quickly as median household incomes, according to a Commonwealth Fund brief.

“The key question is how to slow health care cost growth in a way that benefits middle class and lower-wage working families — that is, keeping premium growth in check without eroding benefits,” the Commonwealth brief states.

“The challenge to policy leaders will be to pursue reforms that improve the quality of health care, rein in cost growth, and ensure that savings are shared with patients and families across the income spectrum.”

ICD-10 reimbursement confidence and preparation levels high

Thirty-six percent of Xtelligent Media readers said they were able to confidently estimate ICD-10’s upcoming impact on reimbursement. But twenty-six percent confirmed they were unable to do so.

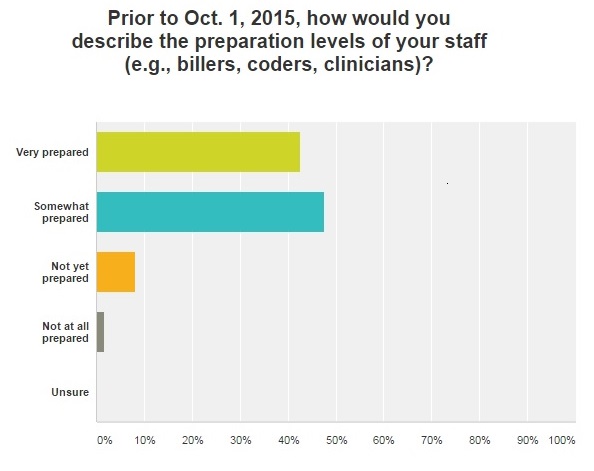

Levels of staff preparation efforts among billers, coders, clinicians, and the like were reportedly high before ICD-10 implementation swung into gear. Ninety percent of readers said their staff was prepared prior to October 1.

Once October 1, 2015 came and went, staff preparation levels reportedly remained very high. Ninety-five percent of readers confirmed they were still indeed prepared for ICD-10 implementation endeavors.

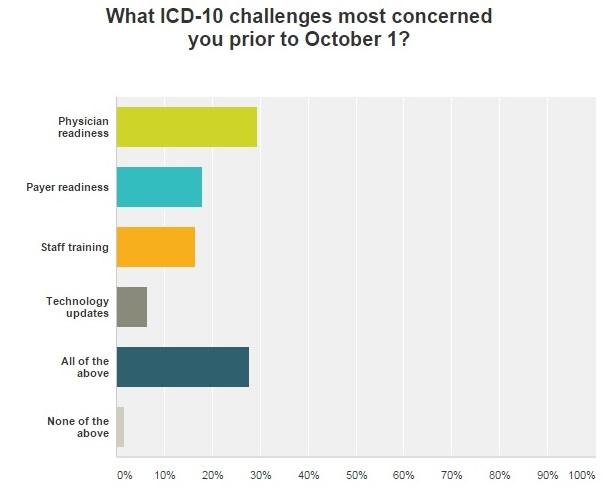

Our readers were most concerned with how physician readiness levels would be impacted with ICD-10 implementation. Levels of payer readiness and staff training were also top concerns.

These findings closely mirror findings from Porter Research and Navicure that 90 percent of healthcare organizations considered themselves adequately prepared for ICD-10.

Value-based initiatives remain a key focus for providers for the remainder of this year, says Porter Research and Navicure. Most providers plan on working on improving revenue cycle management processes this year. Working towards a value-based care model and updating and automating patient collections strategies are other leading concerns for 2016.

Sopurce: http://revcycleintelligence.com/

.png)